put options evaluation using binary tree

In finance, an pick is a contract which conveys to its owner, the holder, the right, but non the obligation, to purchase or sell an underlying asset or musical instrument at a specified strike price on or before a specified date, depending on the style of the selection. Options are typically caused past purchase, as a form of compensation, or as part of a circuitous financial transaction. Thus, they are also a form of asset and have a valuation that may depend on a complex human relationship between underlying nugget value, time until expiration, market place volatility, and other factors. Options may be traded betwixt private parties in over-the-counter (OTC) transactions, or they may be substitution-traded in alive, orderly markets in the grade of standardized contracts.

Definition and application [edit]

An option is a contract that allows the holder the right to buy or sell an underlying asset or financial instrument at a specified strike price on or earlier a specified date, depending on the grade of the option. The strike price may be set by reference to the spot cost (market place price) of the underlying security or commodity on the day an option is issued, or it may be fixed at a discount or at a premium. The issuer has the corresponding obligation to fulfill the transaction (to sell or buy) if the holder "exercises" the option. An option that conveys to the holder the correct to purchase at a specified price is referred to equally a call, while one that conveys the right to sell at a specified price is known as a put.

The issuer may grant an option to a heir-apparent as office of another transaction (such as a share outcome or as part of an employee incentive scheme), or the buyer may pay a premium to the issuer for the option. A call option would ordinarily be exercised just when the strike price is below the marketplace value of the underlying asset, while a put option would normally exist exercised only when the strike price is above the market place value. When an option is exercised, the cost to the option holder is the strike price of the asset acquired plus the premium, if any, paid to the issuer. If the option's expiration date passes without the pick being exercised, the option expires, and the holder forfeits the premium paid to the issuer. In any example, the premium is income to the issuer, and commonly a capital letter loss to the option holder.

The holder of an pick may on-sell the option to a 3rd party in a secondary market, in either an over-the-counter transaction or on an options exchange, depending on the selection. The market toll of an American-mode pick normally closely follows that of the underlying stock beingness the difference between the marketplace toll of the stock and the strike price of the choice. The actual marketplace toll of the pick may vary depending on a number of factors, such as a pregnant option holder needing to sell the selection due to the expiration date approaching and not having the financial resources to exercise the choice, or a heir-apparent in the market trying to aggregate a large pick property. The buying of an option does not generally entitle the holder to any rights associated with the underlying nugget, such as voting rights or any income from the underlying asset, such equally a dividend.

History [edit]

Historical uses of options [edit]

Contracts similar to options take been used since aboriginal times.[one] The showtime reputed option heir-apparent was the ancient Greek mathematician and philosopher Thales of Miletus. On a sure occasion, information technology was predicted that the season'due south olive harvest would exist larger than usual, and during the off-season, he acquired the correct to use a number of olive presses the following spring. When spring came and the olive harvest was larger than expected, he exercised his options and and then rented the presses out at a much higher price than he paid for his 'option'.[ii] [3]

The 1688 book Confusion of Confusions describes the trading of "opsies" on the Amsterdam stock exchange, explaining that "there will be just limited risks to you, while the proceeds may surpass all your imaginings and hopes."[4]

In London, puts and "refusals" (calls) showtime became well-known trading instruments in the 1690s during the reign of William and Mary.[5] Privileges were options sold over the counter in nineteenth century America, with both puts and calls on shares offered by specialized dealers. Their exercise price was stock-still at a rounded-off market cost on the twenty-four hour period or week that the option was bought, and the expiry appointment was generally three months after buy. They were not traded in secondary markets.

In the real estate market, phone call options accept long been used to gather large parcels of land from separate owners; e.thou., a developer pays for the right to buy several side by side plots, but is not obligated to purchase these plots and might non unless they can buy all the plots in the entire bundle.

In the motion picture industry, film or theatrical producers often buy an selection giving the right — but not the obligation — to dramatize a specific volume or script.

Lines of credit requite the potential borrower the correct — but non the obligation — to infringe within a specified time menses.

Many choices, or embedded options, have traditionally been included in bond contracts. For example, many bonds are convertible into common stock at the buyer's selection, or may be called (bought back) at specified prices at the issuer's choice. Mortgage borrowers take long had the option to repay the loan early on, which corresponds to a callable bond option.

Modern stock options [edit]

Options contracts have been known for decades. The Chicago Board Options Commutation was established in 1973, which prepare a regime using standardized forms and terms and merchandise through a guaranteed clearing business firm. Trading activity and academic interest has increased since so.

Today, many options are created in a standardized form and traded through clearing houses on regulated options exchanges, while other over-the-counter options are written as bilateral, customized contracts between a unmarried buyer and seller, ane or both of which may be a dealer or market place-maker. Options are part of a larger class of financial instruments known as derivative products, or just, derivatives.[6] [7]

Contract specifications [edit]

A financial option is a contract between two counterparties with the terms of the option specified in a term sheet. Option contracts may be quite complicated; however, at minimum, they usually contain the following specifications:[8]

- whether the choice holder has the right to purchase (a telephone call option) or the right to sell (a put option)

- the quantity and class of the underlying nugget(s) (east.g., 100 shares of XYZ Co. B stock)

- the strike cost, also known equally the exercise price, which is the price at which the underlying transaction will occur upon exercise

- the expiration appointment, or expiry, which is the last date the option can be exercised

- the settlement terms, for case whether the writer must deliver the bodily asset on do, or may only tender the equivalent cash corporeality

- the terms by which the option is quoted in the marketplace to convert the quoted price into the actual premium – the total corporeality paid by the holder to the writer

Option trading [edit]

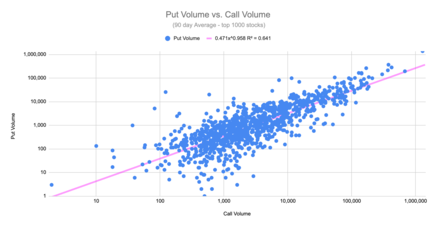

Put Volume vs. Call Volume (xc Day Boilerplate Book)

Forms of trading [edit]

Commutation-traded options [edit]

Commutation-traded options (likewise called "listed options") are a grade of exchange-traded derivatives. Exchange-traded options have standardized contracts, and are settled through a clearing firm with fulfillment guaranteed by the Options Clearing Corporation (OCC). Since the contracts are standardized, accurate pricing models are often available. Exchange-traded options include:[9] [10]

- Stock options

- Bond options and other interest rate options

- Stock market index options or, but, index options and

- Options on futures contracts

- Callable bull/bear contract

![]()

Average Choice Volume (xc days) vs Market Capitalization

Over-the-counter options [edit]

Over-the-counter options (OTC options, also called "dealer options") are traded between two private parties, and are not listed on an exchange. The terms of an OTC pick are unrestricted and may exist individually tailored to meet whatsoever business need. In general, the option writer is a well-capitalized institution (in order to forestall the credit hazard). Option types normally traded over the counter include:

- Interest charge per unit options

- Currency cantankerous charge per unit options, and

- Options on swaps or swaptions.

Past avoiding an exchange, users of OTC options tin narrowly tailor the terms of the option contract to suit individual business requirements. In improver, OTC option transactions more often than not do not need to be advertised to the market place and face up niggling or no regulatory requirements. However, OTC counterparties must establish credit lines with each other, and accommodate to each other'southward clearing and settlement procedures.

With few exceptions,[11] there are no secondary markets for employee stock options. These must either be exercised by the original grantee or immune to elapse.

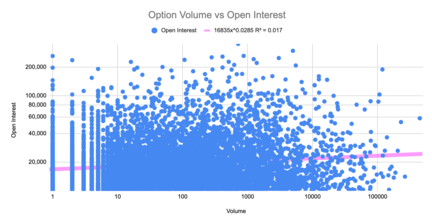

Option Volume vs Open Interest (for 7000+ Contracts)

Substitution trading [edit]

The most common way to trade options is via standardized options contracts that are listed by various futures and options exchanges. [12] Listings and prices are tracked and can exist looked upward by ticker symbol. By publishing continuous, alive markets for choice prices, an exchange enables independent parties to engage in price discovery and execute transactions. Every bit an intermediary to both sides of the transaction, the benefits the commutation provides to the transaction include:

- Fulfillment of the contract is backed by the credit of the substitution, which typically has the highest rating (AAA),

- Counterparties remain bearding,

- Enforcement of market place regulation to ensure fairness and transparency, and

- Maintenance of orderly markets, particularly during fast trading conditions.

Days till Expiration vs Option Volume (7000+ contracts)

Bones trades (American way) [edit]

These trades are described from the point of view of a speculator. If they are combined with other positions, they can as well exist used in hedging. An option contract in US markets usually represents 100 shares of the underlying security.[13] [14]

Long call [edit]

Payoff from buying a call.

A trader who expects a stock's toll to increase tin buy a call pick to purchase the stock at a fixed price (strike price) at a afterward date, rather than purchase the stock outright. The cash outlay on the option is the premium. The trader would take no obligation to buy the stock, but just has the right to do so on or before the expiration date. The hazard of loss would be limited to the premium paid, unlike the possible loss had the stock been bought outright.

The holder of an American-way call option can sell the option holding at whatsoever time until the expiration date, and would consider doing so when the stock's spot price is above the practice price, especially if the holder expects the price of the option to drop. Past selling the selection early on in that situation, the trader tin realise an immediate profit. Alternatively, the trader tin exercise the option — for case, if at that place is no secondary market for the options — then sell the stock, realising a turn a profit. A trader would make a turn a profit if the spot cost of the shares rises by more than than the premium. For example, if the exercise toll is 100 and premium paid is 10, then if the spot price of 100 rises to only 110 the transaction is pause-even; an increase in stock cost above 110 produces a turn a profit.

If the stock price at expiration is lower than the practice price, the holder of the option at that time will allow the phone call contract expire and lose simply the premium (or the price paid on transfer).

Long put [edit]

A trader who expects a stock's cost to decrease can buy a put option to sell the stock at a stock-still price (strike price) at a after date. The trader is nether no obligation to sell the stock, just has the right to practice so on or before the expiration date. If the stock price at expiration is below the do price past more than than the premium paid, the trader makes a profit. If the stock cost at expiration is above the practice price, the trader lets the put contract expire, and loses only the premium paid. In the transaction, the premium as well plays a role every bit information technology enhances the break-even bespeak. For case, if the exercise price is 100 and the premium paid is ten, then a spot price between 90 and 100 is non profitable. The trader makes a turn a profit only if the spot price is below ninety.

The trader exercising a put pick on a stock does not demand to ain the underlying asset, because most stocks can be shorted.

Brusque call [edit]

Payoff from writing a telephone call.

A trader who expects a stock's price to decrease tin sell the stock brusk or instead sell, or "write", a telephone call. The trader selling a phone call has an obligation to sell the stock to the call heir-apparent at a fixed toll ("strike cost"). If the seller does not own the stock when the option is exercised, they are obligated to purchase the stock in the market at the prevailing market cost. If the stock price decreases, the seller of the telephone call (telephone call writer) makes a turn a profit in the corporeality of the premium. If the stock toll increases over the strike price by more than the amount of the premium, the seller loses money, with the potential loss being unlimited.

Brusk put [edit]

Payoff from writing a put.

A trader who expects a stock'south price to increase can purchase the stock or instead sell, or "write", a put. The trader selling a put has an obligation to buy the stock from the put buyer at a stock-still price ("strike price"). If the stock cost at expiration is to a higher place the strike cost, the seller of the put (put writer) makes a profit in the amount of the premium. If the stock price at expiration is below the strike toll by more than than the corporeality of the premium, the trader loses money, with the potential loss beingness up to the strike cost minus the premium. A benchmark index for the performance of a cash-secured curt put option position is the CBOE S&P 500 PutWrite Index (ticker PUT).

Options strategies [edit]

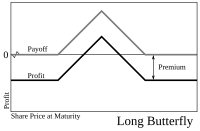

Payoffs from ownership a butterfly spread.

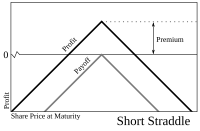

Payoffs from selling a straddle.

Payoffs from a covered telephone call.

Combining whatsoever of the 4 basic kinds of option trades (possibly with different practise prices and maturities) and the 2 bones kinds of stock trades (long and brusk) allows a multifariousness of options strategies. Elementary strategies usually combine only a few trades, while more than complicated strategies can combine several.

Strategies are often used to engineer a particular risk profile to movements in the underlying security. For instance, ownership a butterfly spread (long one X1 call, short two X2 calls, and long one X3 telephone call) allows a trader to profit if the stock price on the expiration engagement is about the middle exercise price, X2, and does not expose the trader to a large loss.

An fe condor is a strategy that is similar to a butterfly spread, but with different strikes for the short options – offering a larger likelihood of profit but with a lower cyberspace credit compared to the butterfly spread.

Selling a straddle (selling both a put and a call at the aforementioned exercise price) would requite a trader a greater turn a profit than a butterfly if the final stock price is nigh the exercise price, but might result in a big loss.

Similar to the straddle is the strangle which is also synthetic by a telephone call and a put, only whose strikes are different, reducing the net debit of the trade, just also reducing the hazard of loss in the trade.

One well-known strategy is the covered call, in which a trader buys a stock (or holds a previously-purchased long stock position), and sells a call. If the stock price rises in a higher place the do price, the call volition exist exercised and the trader will get a fixed profit. If the stock price falls, the phone call volition not be exercised, and whatever loss incurred to the trader will be partially offset by the premium received from selling the call. Overall, the payoffs match the payoffs from selling a put. This relationship is known as put–call parity and offers insights for financial theory. A benchmark index for the performance of a buy-write strategy is the CBOE Due south&P 500 BuyWrite Alphabetize (ticker symbol BXM).

Another very common strategy is the protective put, in which a trader buys a stock (or holds a previously-purchased long stock position), and buys a put. This strategy acts as an insurance when investing on the underlying stock, hedging the investor'southward potential losses, merely too shrinking an otherwise larger profit, if only purchasing the stock without the put. The maximum profit of a protective put is theoretically unlimited every bit the strategy involves being long on the underlying stock. The maximum loss is limited to the purchase price of the underlying stock less the strike cost of the put option and the premium paid. A protective put is besides known as a married put.

Types [edit]

Options can be classified in a few means.

According to the option rights [edit]

- Call options give the holder the correct—but not the obligation—to purchase something at a specific price for a specific fourth dimension catamenia.

- Put options give the holder the correct—but non the obligation—to sell something at a specific toll for a specific fourth dimension catamenia.

According to the underlying assets [edit]

- Equity choice

- Bond option

- Future selection

- Index option

- Commodity option

- Currency option

- Swap option

Other selection types [edit]

Another important grade of options, specially in the U.South., are employee stock options, which are awarded past a company to their employees as a form of incentive bounty. Other types of options be in many financial contracts, for example existent estate options are ofttimes used to gather large parcels of land, and prepayment options are normally included in mortgage loans. Withal, many of the valuation and take chances management principles utilize across all financial options. In that location are two more types of options; covered and naked.[15]

Selection styles [edit]

Options are classified into a number of styles, the most common of which are:

- American option – an option that may be exercised on any trading mean solar day on or before expiration.

- European option – an option that may only exist exercised on decease.

These are ofttimes described as vanilla options. Other styles include:

- Bermudan choice – an option that may exist exercised simply on specified dates on or earlier expiration.

- Asian choice – an selection whose payoff is determined past the average underlying toll over some preset time menses.

- Barrier option – whatever option with the general feature that the underlying security's cost must pass a certain level or "barrier" before it can be exercised.

- Binary option – An all-or-nix choice that pays the full corporeality if the underlying security meets the defined condition on expiration otherwise information technology expires.

- Exotic choice – whatever of a broad category of options that may include circuitous financial structures.[16]

Valuation [edit]

Because the values of option contracts depend on a number of different variables in addition to the value of the underlying asset, they are complex to value. At that place are many pricing models in use, although all essentially contain the concepts of rational pricing (i.eastward. hazard neutrality), moneyness, option time value, and put–call parity.

The valuation itself combines a model of the behavior ("procedure") of the underlying price with a mathematical method which returns the premium as a function of the assumed beliefs. The models range from the (prototypical) Blackness–Scholes model for equities,[17] [ unreliable source? ] [18] to the Heath–Jarrow–Morton framework for interest rates, to the Heston model where volatility itself is considered stochastic. Run into Asset pricing for a list of the diverse models here.

Basic decomposition [edit]

In its most basic terms, the value of an option is commonly decomposed into two parts:

- The first function is the intrinsic value, which is defined as the difference betwixt the market value of the underlying, and the strike price of the given choice

- The second part is the time value, which depends on a set up of other factors which, through a multi-variable, non-linear interrelationship, reflect the discounted expected value of that divergence at expiration.

Valuation models [edit]

As in a higher place, the value of the choice is estimated using a diverseness of quantitative techniques, all based on the principle of take chances-neutral pricing, and using stochastic calculus in their solution. The near basic model is the Black–Scholes model. More sophisticated models are used to model the volatility grin. These models are implemented using a diverseness of numerical techniques.[19] In full general, standard choice valuation models depend on the post-obit factors:

- The current market cost of the underlying security

- The strike price of the option, peculiarly in relation to the current market place price of the underlying (in the money vs. out of the money)

- The cost of holding a position in the underlying security, including interest and dividends

- The time to expiration together with any restrictions on when exercise may occur

- an estimate of the futurity volatility of the underlying security's price over the life of the option

More advanced models tin require additional factors, such equally an approximate of how volatility changes over fourth dimension and for various underlying price levels, or the dynamics of stochastic involvement rates.

The post-obit are some of the principal valuation techniques used in practice to evaluate option contracts.

Black–Scholes [edit]

Following early work by Louis Bachelier and later piece of work by Robert C. Merton, Fischer Black and Myron Scholes made a major quantum by deriving a differential equation that must be satisfied by the cost of any derivative dependent on a non-dividend-paying stock. By employing the technique of amalgam a risk neutral portfolio that replicates the returns of belongings an selection, Black and Scholes produced a closed-grade solution for a European option's theoretical price.[xx] At the aforementioned time, the model generates hedge parameters necessary for effective risk management of option holdings.

While the ideas behind the Black–Scholes model were footing-breaking and eventually led to Scholes and Merton receiving the Swedish Primal Depository financial institution'southward associated Prize for Achievement in Economics (a.m.a., the Nobel Prize in Economics),[21] the application of the model in bodily options trading is impuissant because of the assumptions of continuous trading, constant volatility, and a constant interest rate. Even so, the Blackness–Scholes model is still one of the well-nigh important methods and foundations for the existing financial market in which the result is within the reasonable range.[22]

Stochastic volatility models [edit]

Since the market crash of 1987, it has been observed that market implied volatility for options of lower strike prices are typically higher than for higher strike prices, suggesting that volatility varies both for time and for the price level of the underlying security – a then-called volatility smiling; and with a time dimension, a volatility surface.

The chief approach here is to care for volatility every bit stochastic, with the resultant Stochastic volatility models, and the Heston model as prototype;[23] see #Risk-neutral_measure for a word of the logic. Other models include the CEV and SABR volatility models. Ane main advantage of the Heston model, however, is that it tin can exist solved in closed-form, while other stochastic volatility models require complex numerical methods.[23]

An alternating, though related, approach is to employ a local volatility model, where volatility is treated as a deterministic function of both the current nugget level and of time . Every bit such, a local volatility model is a generalisation of the Black–Scholes model, where the volatility is a constant. The concept was adult when Bruno Dupire[24] and Emanuel Derman and Iraj Kani[25] noted that in that location is a unique diffusion process consequent with the risk neutral densities derived from the market prices of European options. See #Development for word.

Brusque-rate models [edit]

For the valuation of bond options, swaptions (i.e. options on swaps), and interest rate cap and floors (effectively options on the interest rate) various short-rate models take been adult (applicable, in fact, to interest rate derivatives mostly). The best known of these are Black-Derman-Toy and Hull–White.[26] These models describe the future evolution of involvement rates by describing the futurity evolution of the brusque rate. The other major framework for interest rate modelling is the Heath–Jarrow–Morton framework (HJM). The stardom is that HJM gives an analytical description of the entire yield bend, rather than merely the short rate. (The HJM framework incorporates the Brace–Gatarek–Musiela model and market place models. And some of the short rate models can be straightforwardly expressed in the HJM framework.) For some purposes, east.g., valuation of mortgage-backed securities, this can be a big simplification; regardless, the framework is oft preferred for models of college dimension. Note that for the simpler options here, i.e. those mentioned initially, the Blackness model can instead exist employed, with certain assumptions.

Model implementation [edit]

One time a valuation model has been chosen, in that location are a number of dissimilar techniques used to implement the models.

Analytic techniques [edit]

In some cases, i tin take the mathematical model and using belittling methods, develop closed form solutions such every bit the Blackness–Scholes model and the Black model. The resulting solutions are readily computable, as are their "Greeks". Although the Curl–Geske–Whaley model applies to an American telephone call with one dividend, for other cases of American options, closed form solutions are not bachelor; approximations hither include Barone-Adesi and Whaley, Bjerksund and Stensland and others.

Binomial tree pricing model [edit]

Closely following the derivation of Black and Scholes, John Cox, Stephen Ross and Marking Rubinstein developed the original version of the binomial options pricing model.[27] [28] It models the dynamics of the choice's theoretical value for discrete time intervals over the option'due south life. The model starts with a binomial tree of discrete future possible underlying stock prices. By constructing a riskless portfolio of an selection and stock (as in the Black–Scholes model) a simple formula can be used to find the choice toll at each node in the tree. This value tin can judge the theoretical value produced by Blackness–Scholes, to the desired degree of precision. All the same, the binomial model is considered more accurate than Black–Scholes considering information technology is more flexible; e.yard., discrete future dividend payments tin be modeled correctly at the proper forrad time steps, and American options can be modeled also as European ones. Binomial models are widely used past professional pick traders. The Trinomial tree is a similar model, assuasive for an upwardly, down or stable path; although considered more authentic, particularly when fewer time-steps are modelled, it is less commonly used as its implementation is more than complex. For a more full general give-and-take, as well as for application to bolt, interest rates and hybrid instruments, see Lattice model (finance).

Monte Carlo models [edit]

For many classes of options, traditional valuation techniques are intractable because of the complexity of the instrument. In these cases, a Monte Carlo approach may often be useful. Rather than attempt to solve the differential equations of motility that describe the option'southward value in relation to the underlying security's cost, a Monte Carlo model uses simulation to generate random toll paths of the underlying asset, each of which results in a payoff for the choice. The average of these payoffs tin can exist discounted to yield an expectation value for the option.[29] Note though, that despite its flexibility, using simulation for American styled options is somewhat more than circuitous than for lattice based models.

Finite difference models [edit]

The equations used to model the option are oft expressed every bit fractional differential equations (see for example Blackness–Scholes equation). In one case expressed in this course, a finite deviation model tin can exist derived, and the valuation obtained. A number of implementations of finite divergence methods exist for option valuation, including: explicit finite difference, implicit finite difference and the Crank–Nicolson method. A trinomial tree selection pricing model can exist shown to be a simplified application of the explicit finite difference method. Although the finite departure arroyo is mathematically sophisticated, it is particularly useful where changes are assumed over fourth dimension in model inputs – for instance dividend yield, chance-free rate, or volatility, or some combination of these – that are non tractable in closed form.

Other models [edit]

Other numerical implementations which have been used to value options include finite chemical element methods.

Risks [edit]

A telephone call option (too known as a CO) expiring in 99 days on 100 shares of XYZ stock is struck at $fifty, with XYZ currently trading at $48. With future realized volatility over the life of the option estimated at 25%, the theoretical value of the selection is $1.89. The hedge parameters , , , are (0.439, 0.0631, ix.6, and −0.022), respectively. Presume that on the following day, XYZ stock rises to $48.5 and volatility falls to 23.5%. We can calculate the estimated value of the call option by applying the hedge parameters to the new model inputs as:

Under this scenario, the value of the option increases by $0.0614 to $1.9514, realizing a profit of $6.14. Annotation that for a delta neutral portfolio, whereby the trader had also sold 44 shares of XYZ stock as a hedge, the net loss under the aforementioned scenario would be ($15.86).

As with all securities, trading options entails the risk of the option's value changing over time. Withal, unlike traditional securities, the return from property an choice varies non-linearly with the value of the underlying and other factors. Therefore, the risks associated with holding options are more complicated to understand and predict.

In general, the change in the value of an option can be derived from Itô'south lemma as:

where the Greeks , , and are the standard hedge parameters calculated from an choice valuation model, such every bit Black–Scholes, and , and are unit of measurement changes in the underlying's price, the underlying's volatility and fourth dimension, respectively.

Thus, at any bespeak in time, 1 can guess the risk inherent in property an selection past calculating its hedge parameters and and then estimating the expected change in the model inputs, , and , provided the changes in these values are pocket-sized. This technique tin can be used effectively to sympathise and manage the risks associated with standard options. For instance, by offsetting a holding in an pick with the quantity of shares in the underlying, a trader can form a delta neutral portfolio that is hedged from loss for pocket-size changes in the underlying's price. The corresponding toll sensitivity formula for this portfolio is:

Pin risk [edit]

A special state of affairs called pin risk can ascend when the underlying closes at or very close to the option's strike value on the terminal 24-hour interval the option is traded prior to expiration. The option writer (seller) may non know with certainty whether or not the choice will actually be exercised or be immune to expire. Therefore, the option writer may terminate up with a big, unwanted residual position in the underlying when the markets open up on the next trading day after expiration, regardless of his or her best efforts to avoid such a residue.

Counterparty adventure [edit]

A further, frequently ignored, gamble in derivatives such as options is counterparty risk. In an option contract this take chances is that the seller won't sell or buy the underlying asset equally agreed. The chance tin can be minimized by using a financially strong intermediary able to make good on the trade, just in a major panic or crash the number of defaults tin can overwhelm even the strongest intermediaries.

See too [edit]

- American Stock Exchange

- Expanse yield options contract

- Ascot (finance)

- Chicago Lath Options Exchange

- Dilutive security

- Eurex

- Euronext.liffe

- International Securities Exchange

- NYSE Arca

- Philadelphia Stock Commutation

- LEAPS (finance)

- Options backdating

- Options Clearing Corporation

- Options spread

- Options strategy

- Selection symbol

- Real options analysis

- PnL Explained

- Pivot risk (options)

- XVA

References [edit]

- ^ Abraham, Stephan (May thirteen, 2010). "History of Financial Options - Investopedia". Investopedia . Retrieved June 2, 2014.

- ^ Mattias Sander. Bondesson's Representation of the Variance Gamma Model and Monte Carlo Option Pricing. Lunds Tekniska Högskola 2008

- ^ Aristotle. Politics.

- ^ Josef de la Vega. Confusion de Confusiones. 1688. Portions Descriptive of the Amsterdam Stock Exchange Selected and Translated past Professor Hermann Kellenbenz. Baker Library, Harvard Graduate Schoolhouse Of Business Assistants, Boston, Massachusetts.

- ^ Smith, B. Mark (2003), History of the Global Stock Marketplace from Ancient Rome to Silicon Valley, University of Chicago Press, p. 20, ISBN0-226-76404-4

- ^ Brealey, Richard A.; Myers, Stewart (2003), Principles of Corporate Finance (seventh ed.), McGraw-Hill, Chapter 20

- ^ Hull, John C. (2005), Options, Futures and Other Derivatives (excerpt by Fan Zhang) (6th ed.), Pg 6: Prentice-Hall, ISBN0-thirteen-149908-4

{{citation}}: CS1 maint: location (link) - ^ Characteristics and Risks of Standardized Options, Options Immigration Corporation, retrieved July fifteen, 2020

- ^ Merchandise CME Products, Chicago Mercantile Substitution, retrieved June 21, 2007

- ^ ISE Traded Products, International Securities Exchange, archived from the original on May 11, 2007, retrieved June 21, 2007

- ^ Elinor Mills (December 12, 2006), Google unveils unorthodox stock option sale, CNet, retrieved June 19, 2007

- ^ Harris, Larry (2003), Trading and Exchanges, Oxford Academy Printing, pp.26–27

- ^ invest-faq or Law & Valuation for typical size of pick contract

- ^ "Understanding Stock Options" (PDF). The Options Clearing Corporation and CBOE. Retrieved August 27, 2015.

- ^ Lawrence K. McMillan (Feb 15, 2011). McMillan on Options. John Wiley & Sons. pp. 575–. ISBN978-1-118-04588-6.

- ^ Fabozzi, Frank J. (2002). The Handbook of Financial Instruments (1st ed.). New Jersey: John Wiley and Sons. p. 471. ISBN0-471-22092-2.

- ^ Benhamou, Eric. "Options pre-Black Scholes" (PDF).

- ^ Black, Fischer; Scholes, Myron (1973). "The Pricing of Options and Corporate Liabilities". Periodical of Political Economy. 81 (3): 637–654. doi:10.1086/260062. JSTOR 1831029. S2CID 154552078.

- ^ Reilly, Frank Thousand.; Brown, Keith C. (2003). Investment Assay and Portfolio Management (7th ed.). Thomson Southwestern. Chapter 23.

- ^ Black, Fischer and Myron Due south. Scholes. "The Pricing of Options and Corporate Liabilities", Periodical of Political Economy, 81 (three), 637–654 (1973).

- ^ Das, Satyajit (2006), Traders, Guns & Coin: Knowns and unknowns in the dazzling world of derivatives (6th ed.), London: Prentice-Hall, Chapter i 'Financial WMDs – derivatives demagoguery,' p.22, ISBN978-0-273-70474-4

- ^ Hull, John C. (2005), Options, Futures and Other Derivatives (6th ed.), Prentice-Hall, ISBN0-13-149908-iv

- ^ a b Jim Gatheral (2006), The Volatility Surface, A Practitioner'south Guide, Wiley Finance, ISBN978-0-471-79251-two

- ^ Bruno Dupire (1994). "Pricing with a Smile". Risk. "Download media disabled" (PDF). Archived from the original (PDF) on September vii, 2012. Retrieved June 14, 2013.

- ^ Derman, E., Iraj Kani (1994). ""Riding on a Grinning." Gamble, 7(two) Feb.1994, pp. 139-145, pp. 32-39" (PDF). Risk. Archived from the original (PDF) on July x, 2011. Retrieved June 1, 2007. CS1 maint: multiple names: authors listing (link)

- ^ Fixed Income Analysis, p. 410, at Google Books

- ^ Cox, J. C., Ross SA and Rubinstein M. 1979. Options pricing: a simplified approach, Journal of Financial Economics, 7:229–263.[1]

- ^ Cox, John C.; Rubinstein, Marker (1985), Options Markets, Prentice-Hall, Chapter 5

- ^ Crevice, Timothy Falcon (2004), Basic Black–Scholes: Selection Pricing and Trading (1st ed.), pp. 91–102, ISBN0-9700552-2-6

{{citation}}: CS1 maint: location (link)

Further reading [edit]

- Fischer Black and Myron S. Scholes. "The Pricing of Options and Corporate Liabilities," Periodical of Political Economy, 81 (3), 637–654 (1973).

- Feldman, Barry and Dhuv Roy. "Passive Options-Based Investment Strategies: The Case of the CBOE South&P 500 BuyWrite Index." The Periodical of Investing, (Summer 2005).

- Kleinert, Hagen, Path Integrals in Quantum Mechanics, Statistics, Polymer Physics, and Fiscal Markets, quaternary edition, World Scientific (Singapore, 2004); Paperback ISBN 981-238-107-iv (also available online: PDF-files)

- Hill, Joanne, Venkatesh Balasubramanian, Krag (Fizz) Gregory, and Ingrid Tierens. "Finding Blastoff via Covered Index Writing." Fiscal Analysts Journal. (Sept.-October. 2006). pp. 29–46.

- Millman, Gregory J. (2008), "Futures and Options Markets", in David R. Henderson (ed.), Concise Encyclopedia of Economics (2d ed.), Indianapolis: Library of Economics and Freedom, ISBN978-0865976658, OCLC 237794267

- Moran, Matthew. "Risk-adjusted Performance for Derivatives-based Indexes – Tools to Assist Stabilize Returns." The Journal of Indexes. (4th Quarter, 2002) pp. 34–40.

- Reilly, Frank and Keith C. Brown, Investment Analysis and Portfolio Direction, 7th edition, Thompson Southwestern, 2003, pp. 994–5.

- Schneeweis, Thomas, and Richard Spurgin. "The Benefits of Index Choice-Based Strategies for Institutional Portfolios" The Journal of Alternative Investments, (Spring 2001), pp. 44–52.

- Whaley, Robert. "Take a chance and Return of the CBOE BuyWrite Monthly Index" The Journal of Derivatives, (Winter 2002), pp. 35–42.

- Bloss, Michael; Ernst, Dietmar; Häcker Joachim (2008): Derivatives – An authoritative guide to derivatives for financial intermediaries and investors Oldenbourg Verlag München ISBN 978-3-486-58632-9

- Espen Gaarder Haug & Nassim Nicholas Taleb (2008): "Why Nosotros Have Never Used the Black–Scholes–Merton Option Pricing Formula"

Source: https://en.wikipedia.org/wiki/Option_(finance)

Posted by: perezthavou.blogspot.com

0 Response to "put options evaluation using binary tree"

Post a Comment